Quick answer: The 50-30-20 rule allocates your post-tax monthly income as 50% to needs (rent, groceries, utilities, EMIs, transport, insurance), 30% to wants (dining, entertainment, shopping, travel), and 20% to savings and investments (SIPs, emergency fund, retirement). The rule, popularised by Elizabeth Warren in her 2005 book "All Your Worth," is a useful directional framework but the rigid percentages don''t fit all Indian incomes equally. At ₹50,000-80,000 monthly take-home in a metro, "needs" often consume 65-75% of income — making 20% savings genuinely difficult and a more realistic split is 70-15-15. At ₹1-2 lakh monthly, the standard 50-30-20 works well. At ₹2 lakh+ monthly, you should push toward 40-20-40, because lifestyle inflation becomes the bigger enemy than insufficient income. The rule is a target to grow into, not a verdict to apply rigidly from month one. The honest target for any salaried Indian: save something, automate it, and increase the percentage each year as income grows.

Key takeaways

- 50-30-20 is a useful framework but the rigid percentages don''t fit all Indian incomes — adapt the split to your income level rather than forcing your spending into someone else''s template.

- At ₹50,000-80,000 monthly take-home in a metro, a realistic starting split is 70-15-15 because needs (especially rent) consume more of the budget — the standard 50% needs ceiling is unachievable.

- At ₹1.5 lakh+ monthly, you should push beyond 20% savings toward 30-40% — lifestyle inflation is the real enemy at higher incomes, not insufficient earnings.

- EMIs, insurance premiums, and emergency fund contributions count as needs (not wants), regardless of what specific products you spend on.

- The single most important number isn''t the exact percentage — it''s that the savings allocation is automated and increases each year alongside income.

"How much should I save every month?" is one of the most-Googled personal finance questions in India, and the most common answer — the 50-30-20 rule — is also one of the most misleading when applied without adjustment. The rule was designed for American middle-class incomes in the mid-2000s, where the typical household could indeed cover "needs" within 50% of take-home pay. Apply it to a salaried Indian earning ₹60,000 monthly in Mumbai with ₹22,000 of rent, ₹8,000 of groceries, ₹4,000 of transport, ₹3,000 of utilities, and an EMI, and you discover that "needs" already consumes 70% — making the rule''s prescriptions mathematically impossible from the start.

This article explains what the 50-30-20 rule actually means, why the rigid percentages need adjustment for Indian incomes, and what realistic monthly savings looks like at different earning levels. The point isn''t to abandon the framework — it''s genuinely useful — but to apply it as a target to grow into, not a verdict to apply mechanically. The honest practitioner answer to "how much should I save?" is: as much as you sustainably can, automated, and increased every year as your income grows. Use Ganak''s SIP Calculator to model what specific savings amounts compound to over 10, 20, and 30 years.

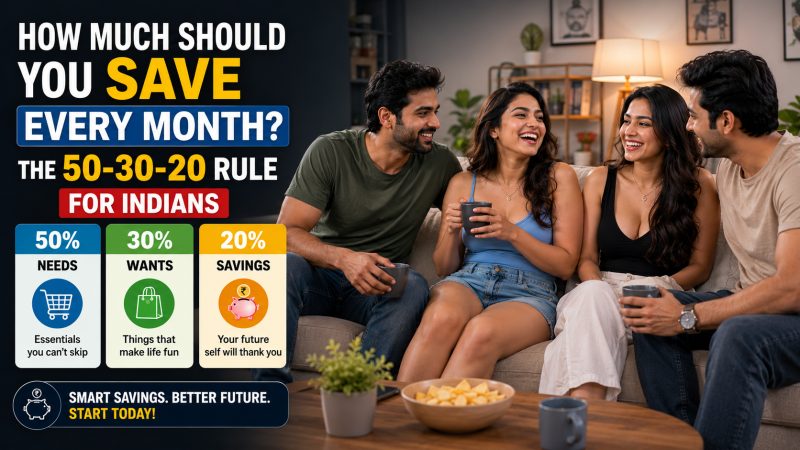

What the 50-30-20 Rule Actually Says

The rule was popularised by then-Harvard professor Elizabeth Warren in her 2005 book All Your Worth: The Ultimate Lifetime Money Plan, co-written with her daughter Amelia Warren Tyagi. It splits your monthly take-home income (after taxes and EPF deductions) into three buckets:

- 50% on Needs: the things you genuinely cannot live without. Rent or home loan EMI, groceries, utilities, basic transport, health insurance, life insurance, minimum debt payments, and essential medical expenses. If you stopped paying for these, your life would collapse within a month or two.

- 30% on Wants: the discretionary purchases that improve quality of life but aren''t strictly necessary. Restaurants, entertainment, streaming subscriptions, vacations, non-essential shopping, hobbies, and the "premium" version of things you''d otherwise buy basic versions of (the OTT bundle vs free YouTube, the gym vs walks in the park, the cab vs the metro).

- 20% on Savings: contributions to investments, emergency fund building, retirement (NPS, EPF voluntary contributions, PPF), and debt repayment beyond the minimums.

The rule''s usefulness is the conceptual clarity it provides. Rather than tracking 47 different expense categories, you only need to know your total spending in three buckets and whether each bucket is roughly in proportion. The split also implicitly defines "savings" as a non-negotiable line item alongside needs — not as "whatever''s left at month-end after spending," which is the failure mode for most non-savers.

The 20% savings target was calibrated to American middle-class incomes where the math worked out. Applied to Indian incomes, the math frequently doesn''t — particularly in metros, where rent alone routinely exceeds 30% of take-home pay even for middle-class earners. This doesn''t mean the rule is useless; it means the percentages need adjustment to your actual income level.

Why the Rigid Percentages Fail at Indian Incomes

The 50% needs ceiling collapses at lower Indian salaried incomes for one structural reason: metro housing costs don''t scale linearly with income. A 2BHK in Bengaluru''s Whitefield or Mumbai''s suburbs rents for ₹25,000-40,000 regardless of whether you earn ₹60,000 or ₹2 lakh per month. At the lower end, that''s 50-65% of your take-home pay before any other need is considered. Add groceries, transport, utilities, and a basic insurance premium, and you''re already at 70-80% of income in "needs" — leaving no realistic path to 20% savings without spending nothing on "wants."

The Worldpanel by Numerator''s 2025 report on Indian household spending found that average urban household quarterly expenses reached ₹73,579 — about ₹24,500 per month per household — with expenses rising 33% over three years. For a single earner supporting that household on a ₹50,000-70,000 income, "wants" become a luxury they may genuinely not be able to afford.

This is why mechanically applying 50-30-20 produces guilt and abandonment rather than financial improvement. A salaried Indian who reads the rule, looks at their actual budget showing 70% needs and 5% savings, and concludes they''ve "failed at money" is more likely to give up on budgeting entirely than to find a path to 20% savings overnight. The honest framework acknowledges this and offers realistic alternatives by income level.

Realistic Allocations by Income Level

The table below shows realistic percentage allocations for different monthly take-home incomes in an Indian metro context, recognising that needs scale less than proportionally with income. These are starting points to work from, not rigid prescriptions — your specific city, family size, and dependents will adjust the exact numbers.

| Monthly take-home | Realistic split | Needs ₹ | Wants ₹ | Savings ₹ | Context |

|---|---|---|---|---|---|

| ₹50,000 | 70-15-15 | ₹35,000 | ₹7,500 | ₹7,500 | Just starting career; 20% savings is genuinely hard in metros |

| ₹80,000 | 65-20-15 | ₹52,000 | ₹16,000 | ₹12,000 | Pushing toward standard rule; needs still high in proportion |

| ₹1,00,000 | 55-25-20 | ₹55,000 | ₹25,000 | ₹20,000 | Standard 50-30-20 within reach; aim here |

| ₹1,50,000 | 45-30-25 | ₹67,500 | ₹45,000 | ₹37,500 | Comfortable middle income; push savings above 20% |

| ₹2,00,000 | 40-30-30 | ₹80,000 | ₹60,000 | ₹60,000 | Senior professional; lifestyle inflation is the enemy |

| ₹3,00,000+ | 35-25-40 | ₹1,05,000 | ₹75,000 | ₹1,20,000 | Aim for 40%+ savings; needs as % keeps falling with income |

Three patterns emerge from this. First, the needs percentage falls steadily as income rises — rent, groceries, and transport don''t scale proportionally with salary increments. Second, the savings percentage should rise with income, not stay frozen at 20%. The investor earning ₹3 lakh per month and still saving only 20% is squandering most of the income advantage; their lifestyle has inflated to absorb the surplus. Third, the wants percentage tends to be remarkably stable across income levels — middle-class urban Indians spend a roughly similar absolute amount on dining, entertainment, and discretionary shopping regardless of whether they earn ₹80,000 or ₹2 lakh.

The Hard Part: Categorising Needs vs Wants

The clean three-bucket framework gets messy in practice. Most spending sits in a gray zone where reasonable people disagree about whether something is a need or a want. A few clarifying principles:

EMIs are needs, not wants. Home loan EMI, car loan EMI, education loan EMI — these are contractual obligations whose default has severe consequences. Even if the underlying asset (the car) was a discretionary purchase, the EMI itself is now a need. The same goes for credit card minimum payments, though paying only the minimum on credit card debt is a different financial crisis that we''ll cover separately.

Insurance premiums are needs. Term life insurance (if you have dependents), health insurance, motor insurance for any vehicle you drive — all needs. Endowment policies and ULIPs are wants (or arguably mistakes) because they''re investments dressed up as insurance, not actual protection.

The "premium" version of a need is a want. Groceries from the local kirana are a need; gourmet groceries from a premium delivery app are partly a want. A basic Maruti Swift is transport (need); a luxury sedan is partly a want. The base level — what you''d need to function — is the need bucket; the premium delta is wants.

OTT subscriptions, gym memberships, streaming services are wants. Even if you genuinely use them every day, they''re not essential to maintaining life or work. Useful, valuable, often worth keeping — but in the wants bucket.

Children''s education is mostly a need. School fees, books, tuition for required subjects are needs. Premium activities (multiple coaching classes, expensive extracurriculars) sit in a gray zone — culturally treated as needs in India, technically wants in the strict framework. Most families consciously allocate them as needs and adjust other categories.

Emergency fund contributions are savings, not needs. Until your emergency fund is fully built (3-6 months of expenses, as we''ll cover in the next article), every rupee going to it counts toward your 15-20% savings allocation.

Where the 20% Savings Should Actually Go

The savings bucket isn''t a single destination — it should be allocated across the financial hierarchy covered in the Beginner''s Guide to Investing pillar. The order of operations within the savings allocation:

- Emergency fund first. Until you have 3-6 months of essential expenses set aside in a liquid form, the entire savings allocation goes here. Stop everything else until this is built.

- Health and term life insurance. Premiums are paid from the needs bucket (above), but ensuring adequate coverage is part of building the foundation.

- Retirement: EPF + NPS + PPF. Your EPF contribution (12% of basic salary, mandatory) handles part of this automatically. Add NPS contribution for the additional ₹50,000 deduction (Section 80CCD(1B)) if you''re in the old regime. PPF contributions of up to ₹1.5 lakh per year work for both regimes.

- Equity SIPs for long-term wealth. Once the foundation is in place, the bulk of monthly savings should go into low-cost equity index funds via SIP. This is the wealth-building engine for any horizon beyond 7 years.

- Goal-based allocations. Separate SIPs for specific goals — child''s education, home down payment, retirement corpus.

A practical allocation of a ₹20,000 monthly savings budget for a 30-year-old salaried professional with a fully built emergency fund and no major loans:

- PPF: ₹4,000/month (₹48,000/year, within the ₹1.5L 80C ceiling and earning 7.1% tax-free)

- NPS Tier 1: ₹4,200/month (₹50,400/year, claiming the full Section 80CCD(1B) ₹50,000 deduction)

- Equity index fund SIP: ₹10,000/month (long-term wealth building)

- Liquid fund / sweep FD: ₹1,800/month (topping up emergency fund as expenses grow)

This split builds simultaneous tax efficiency (₹98,400 of annual deductions), retirement weighting (PPF + NPS), wealth-building (equity SIP), and continued buffer growth.

Variations on the Rule

Several adaptations of 50-30-20 are worth knowing:

60-20-20 (Aggressive saver variant). Compresses wants to 20% to push savings to 20% even when needs run high. Works well for early-career professionals who are still building their lifestyle and can compress discretionary spending willingly.

50-30-20-10 (Charitable variant). Adds a fourth bucket for charitable giving or family support — common among Indian professionals supporting parents or extended family. Pulls equally from needs (which sometimes overlaps with family support) and wants.

70-20-10 (Survival mode). The honest starting framework for ₹40,000-60,000 monthly incomes in metros. Doesn''t pretend 20% savings is achievable; sets a realistic 10% target with the understanding that this will increase as income grows. Better to actually save 10% than aspire to 20% and save 0%.

FIRE-aligned variant (40-20-40 or 30-20-50). Aggressive savings targeted at financial independence — typically pursued by high-earning professionals consciously aiming for early retirement. Requires consistently keeping lifestyle inflation contained.

None of these is "correct" or "wrong." The right framework is the one you can sustain over years, not the one that looks best in a budget spreadsheet for one month.

Common Mistakes When Applying the Rule

Specific failure patterns to avoid:

Forcing yourself into the rigid 50-30-20 percentages when your income makes it impossible. Trying to spend less than 50% on needs when your rent alone is 40% of your salary produces frustration and budgeting fatigue. Accept the reality of your current income level, set a realistic starting split (70-15-15 if needed), and aim to improve the split over time as income grows.

Treating savings as the residual after spending. "I''ll save whatever''s left at month-end" produces near-zero savings for almost everyone. Reverse the order: pay yourself first by setting up an auto-debit SIP that runs on the 5th of every month, then spend what remains. The same money, ordered differently, produces dramatically different outcomes.

Lifestyle inflation as income rises. The most common failure mode for high earners. A ₹50,000 earner who graduates to ₹2 lakh per month should not be saving the same percentage as before — they should be saving a much higher percentage. If your savings percentage doesn''t rise with your salary, you''re absorbing the entire raise into "wants" and your wealth-building trajectory stalls.

Counting "wants" as "needs" to make the math work. If you classify your annual vacation, OTT subscriptions, restaurant meals, and gym membership all as "needs," you''ve broken the framework. The discipline of the rule is the honest categorisation. Wants are real, valuable, and worth spending money on — just call them what they are.

Spending the "wants" bucket on lifestyle inflation rather than experiences. The wants budget is best spent on things that produce lasting value or memories — travel, experiences, hobbies — rather than on lifestyle creep (a slightly bigger car, a slightly fancier neighbourhood, a slightly more premium phone) that you adapt to within months and no longer notice. The same ₹30,000/month spent on wants can produce a great trip or a slightly more expensive monthly bill — they''re very different uses of the same money.

Frequently Asked Questions

What is the 50-30-20 rule?

The 50-30-20 rule allocates your monthly post-tax income into three buckets: 50% to needs (rent, groceries, utilities, EMIs, insurance, transport), 30% to wants (dining, entertainment, shopping, travel), and 20% to savings and investments (SIPs, emergency fund, retirement). The rule was popularised by Elizabeth Warren in her 2005 book "All Your Worth" as a simple framework for budgeting without tracking dozens of categories. It''s a useful directional guide, but the rigid percentages don''t fit all Indian incomes equally — at lower metro incomes, "needs" frequently exceed 50%, requiring an adapted framework like 70-15-15.

How much should I save every month in India?

Aim for at least 15-20% of your monthly take-home income, with the percentage rising as income grows. For a ₹50,000 monthly earner in a metro, even 10-15% (₹5,000-7,500/month) is a realistic start. For a ₹1 lakh earner, 20% (₹20,000/month) becomes achievable. For a ₹2 lakh+ earner, push toward 30-40% — lifestyle inflation at higher incomes is the bigger threat than insufficient earnings. The single most important number isn''t the exact percentage; it''s that you automate the savings via auto-debit SIPs and increase the amount each year as income rises.

Why doesn''t 50-30-20 work for lower Indian incomes?

Because metro housing costs and basic living expenses don''t scale linearly with income. A 2BHK in Bengaluru or Mumbai rents for ₹25,000-40,000 regardless of whether you earn ₹60,000 or ₹2 lakh per month. At ₹60,000 income, that''s 40-65% of take-home pay just for rent, before groceries, utilities, or transport. By the time all genuine needs are covered, "needs" can consume 70-80% of income, making the rule''s 50% needs ceiling mathematically impossible. The honest adaptation for ₹50,000-80,000 monthly incomes is a 70-15-15 or 65-20-15 split, with the savings percentage rising as income grows.

Are EMIs needs or wants?

EMIs are needs, regardless of whether the underlying asset (the car, the home, the appliance) was a discretionary purchase. Once you''ve signed a loan, the EMI is a contractual obligation whose default has severe credit and legal consequences — making the payment non-negotiable. The same goes for credit card minimum payments. Insurance premiums (term life if you have dependents, health insurance, motor insurance for vehicles you drive) are also needs. Endowment policies and ULIPs sold as "insurance" are technically wants because they''re investments dressed up as insurance, not actual protection.

Should I save 20% if I have credit card debt?

No. If you have credit card debt at 30-40% annual interest, every rupee should go to paying it off before starting equity investments. The math is straightforward: paying off a 36% credit card debt is a guaranteed 36% return — better than any equity investment can offer over similar horizons. Maintain the emergency fund (at smaller size — 1-2 months of expenses initially), keep insurance premiums current, and direct everything else to credit card payoff. Once the debt is cleared, redirect the same monthly amount to SIPs. The 50-30-20 rule assumes you''re not paying high-interest debt; if you are, that debt is the priority.

Where should the 20% savings actually go?

The savings bucket should be allocated across a financial hierarchy: (1) emergency fund first until you have 3-6 months of expenses, (2) insurance premiums for term life and health (typically paid from the needs bucket), (3) retirement contributions to EPF, NPS, and PPF for tax efficiency and forced retirement weighting, (4) equity SIPs for long-term wealth building, (5) goal-based allocations for specific goals like education or home purchase. A practical ₹20,000 monthly savings allocation for a 30-year-old with a built emergency fund might be ₹10,000 to an equity index fund SIP, ₹4,200 to NPS, ₹4,000 to PPF, and ₹1,800 to top up the emergency fund as expenses grow.

What''s the right savings rate for higher incomes?

Aggressively above 20%. A salaried professional earning ₹2 lakh+ per month should target 30-40% savings rates, not the standard 20%. The reason: at higher incomes, needs as a percentage of income falls naturally (rent, groceries, transport don''t scale proportionally with salary), so the surplus goes either to wants or to savings. If your savings rate doesn''t rise with income, you''re absorbing the entire raise into lifestyle inflation — the same lifestyle that felt luxurious at ₹1 lakh feels normal at ₹2 lakh feels inadequate at ₹3 lakh. The discipline at higher incomes is to consciously cap lifestyle and direct the surplus to wealth-building, not to absorb the entire raise into a bigger flat, fancier car, and more expensive holidays.

Sources and Further Reading

This article references the 50-30-20 rule popularised by Elizabeth Warren and Amelia Warren Tyagi in All Your Worth: The Ultimate Lifetime Money Plan (2005), RBI Handbook of Statistics on the Indian Economy 2025 for household savings data, and Worldpanel by Numerator''s 2025 report on Indian household spending patterns. For data and official references:

- Reserve Bank of India — Handbook of Statistics on the Indian Economy

- AMFI — Association of Mutual Funds in India, investor education resources

- SEBI — Investor education on systematic investing and goal planning

- EPFO — Employees'' Provident Fund Organisation, contribution and benefit details

Last verified: 27 May 2026. The realistic percentage allocations above are framework starting points; specific allocations should reflect your city, family situation, dependents, and stage of career. Adjustments to taxation, basic deduction limits, or major policy changes affecting take-home income may shift these splits over time.